A More Constructive Spring Market Begins to Take Shape

April brought a more encouraging tone to the Toronto and GTA real estate market, with sales activity improving year-over-year while the number of new listings declined. Although prices remain below last year’s levels, the data suggests that the market may be moving through the early stages of stabilization. Buyers are still selective and value-conscious, but there is a noticeable increase in activity as lower prices and improved borrowing conditions begin to bring some confidence back into the market.

Across the GTA, 5,946 homes sold in April, representing a 7% increase compared with April 2025. At the same time, 17,097 new listings came to market, down 9.3% year-over-year. This combination of higher sales and fewer new listings is important because it suggests that overall market conditions tightened during the first full month of the spring market. On a seasonally adjusted basis, both sales and new listings were up from March, but sales increased at a faster pace, pointing to more competition in certain neighbourhoods and property segments.

Pricing, however, continues to reflect a market where buyers still have meaningful leverage. The average GTA selling price was $1,051,969 in April, down 4.9% from April 2025, while the MLS Home Price Index Composite benchmark declined 6.6% year-over-year. That said, the month-over-month picture was more constructive. The seasonally adjusted average selling price edged higher from March, while the benchmark price held steady. In practical terms, this suggests that while annual comparisons remain soft, the pace of price declines may be moderating.

“We have experienced an uptick in home buying activity so far this spring. Buyers have taken advantage of more affordable housing market conditions on the back of lower home prices. If market conditions continue to tighten and home prices level off, this could be a signal to intending homebuyers who remain on the sidelines,” said TRREB President Daniel Steinfeld.

This is the nuance of the current market. We are not yet in a broadly rising market, but we are also no longer seeing the same degree of hesitation that characterized much of the past year. Buyers are responding to improved affordability relative to last spring, but they are still disciplined. Well-positioned properties are receiving attention, while homes that are not priced in line with current market conditions continue to sit. Strategy remains critical.

The City of Toronto showed stronger momentum than the broader 905 region in April. Toronto recorded 2,312 sales, up from 2,118 a year earlier, while the average selling price came in at $1,091,761. New listings in the City declined to 6,136 from 7,108 last April, which helped firm up conditions compared with last year. The 905 region also saw sales increase, with 3,634 transactions compared with 3,438 in April 2025, while the average price was $1,026,653.

The difference between Toronto and the surrounding regions is worth noting. Toronto appears to be benefiting from renewed interest in established urban neighbourhoods, where proximity to transit, amenities, schools, restaurants, cultural institutions, and walkable lifestyle continue to matter. In many cases, buyers who may have moved farther out during the pandemic are reassessing the value of convenience, commute time, and daily lifestyle. This does not mean the City is immune to affordability pressures, but it does suggest that demand for well-located Toronto real estate remains resilient.

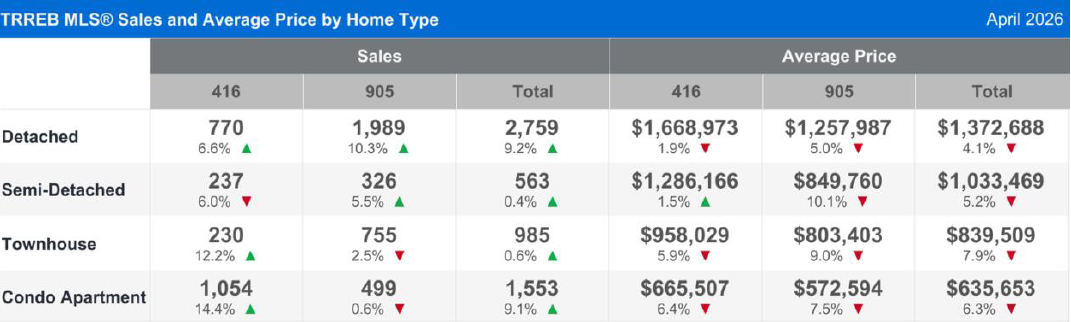

Detached homes were one of the stronger areas of the market in April. Across the GTA, detached sales rose 9.2% year-over-year, with the average detached price at $1,372,688, down 4.1% from last year. In the City of Toronto, detached homes averaged $1,668,973, while detached homes in the 905 averaged $1,257,987. This remains a highly segmented market, with location, condition, lot quality, renovation level, and perceived long-term value all playing a significant role in buyer response.

Semi-detached homes and townhouses were steadier from a sales perspective but continued to show price sensitivity. GTA semi-detached sales were essentially flat year-over-year, while the average price declined to $1,033,469. Townhouse sales were also relatively stable, with the average price at $839,509. These segments remain important for move-up buyers and families seeking more space, but affordability constraints continue to influence how aggressively buyers are prepared to act.

The condominium apartment market also showed signs of improved activity, particularly in the City of Toronto. GTA condo apartment sales rose 9.1% year-over-year, with 1,553 sales in April. In Toronto specifically, condo apartment sales increased 14.4% compared with last April, a notable improvement after a prolonged period of softness. The average GTA condo apartment price was $635,653, while the City of Toronto average was $665,507. Prices remain below last year’s levels, but the increase in sales suggests that buyers are beginning to respond to improved value in the condo segment.

This is especially relevant for first-time buyers, downsizers, and investors who have been waiting for more favourable conditions. The condo market remains price-sensitive, and inventory levels still provide choice. However, if sales continue to improve while new listings trend lower, the current window of negotiating power may begin to narrow over the coming months.

“Lower home prices and borrowing costs over the past year have been a catalyst for some homebuyers this spring. However, we still have a substantial amount of pent-up demand in the marketplace. More certainty on the trade front and an easing in geopolitical tensions would result in further improvements in market activity,” said TRREB’s Chief Information Officer Jason Mercer.

From a broader economic standpoint, borrowing costs remain an important factor. The Bank of Canada held its policy rate at 2.25% on April 29, which provided some stability for borrowers after a period of significant interest rate volatility. Inflation remains an important variable, with Statistics Canada reporting that the Consumer Price Index rose 2.8% year-over-year in April, up from 2.4% in March. While inflationary pressures and global uncertainty continue to influence confidence, the current interest rate environment is more predictable than it was during the peak of the tightening cycle.

Looking ahead, the April results suggest a market that is gradually finding better balance. Buyers still have choice, and in many cases, room to negotiate. Sellers, however, are beginning to benefit from improved activity, particularly where supply has pulled back and where properties are priced realistically. The market is not rewarding aspirational pricing, but it is responding to quality, location, preparation, and a thoughtful pricing strategy.

For buyers, this remains a valuable moment to be active. Prices are still lower than they were a year ago in most major categories, selection remains reasonable, and there is still less urgency than in a heated seller’s market. For sellers, the improvement in sales activity is encouraging, but success depends on reading the market accurately. Presentation, pricing, and timing all matter.

Overall, April marked a positive step forward for the Toronto and GTA market. The recovery is measured rather than dramatic, but the direction is constructive. After many months of caution, buyers are beginning to re-engage, inventory is tightening in some areas, and prices are showing early signs of stabilization. In a market like this, informed strategy is essential, and the best opportunities are often found by looking beyond the headline numbers to understand how conditions are shifting by neighbourhood, property type, and price point.