A Spring Market Finding Its Footing

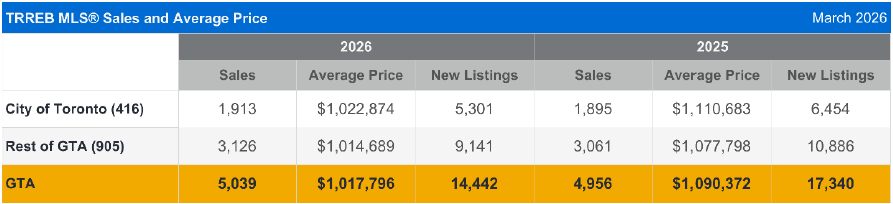

March brought a modest shift in tone to the Greater Toronto Area (GTA) housing market. After a slow start to the year, the spring market began to show more life, with sales improving both month over month and slightly year over year. According to the Toronto Regional Real Estate Board (TRREB), GTA home sales reached 5,039 in March, up 1.7% compared to March 2025, while the average selling price came in at $1,017,796, down 6.7% from a year ago. The MLS Home Price Index benchmark was also down 7.4% annually, reinforcing that while activity has strengthened, pricing remains softer than it was last spring.

“It’s encouraging to see an uptick in March home sales compared to last month and last year. This suggests that an increasing number of GTA households are looking to take advantage of improved affordability as we move into the spring market. Positive news on trade and geopolitical issues would help improve consumer confidence and home sales in the months ahead,” said TRREB President Daniel Steinfeld.

What made March particularly notable was the change in supply. New listings declined sharply to 14,442, down 16.7% year over year, while sales rose at a slightly faster pace than new listings on a seasonally adjusted basis. This created a modest tightening in market conditions and offered an early indication that the imbalance favouring buyers may be beginning to narrow. That said, this is not yet a strong seller’s market. Inventory remains elevated by longer-term standards, and buyers continue to benefit from meaningful negotiating power in most segments. Homes sold, on average, for 98% of the asking price, and days on market remained higher than last year.

In many respects, March can best be described as a stabilizing month rather than a turning point. As one would expect, the spring market delivered a seasonal lift in activity, and there are signs that improved borrowing conditions have brought some buyers back into the market. However, affordability remains a central challenge, particularly in Toronto, and economic uncertainty continues to influence decision-making. Buyers are active, but highly selective. They are responding when they perceive value, but they remain measured and disciplined in their approach.

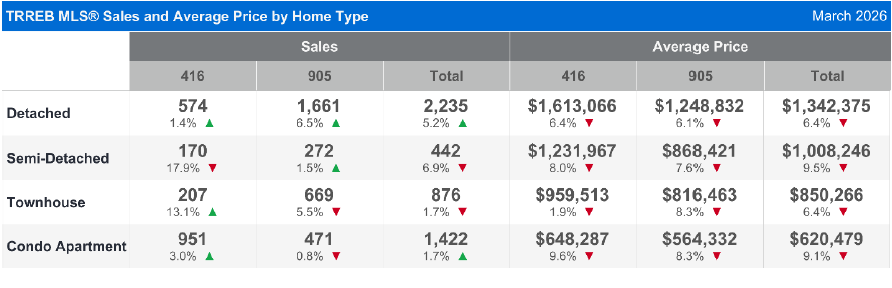

Across property types, the market remains uneven. Detached homes continued to show relative resilience in March, with average prices rising modestly from February and sales volumes improving. Freehold townhomes also appeared comparatively stable. By contrast, semis and condominium apartments remained under greater pressure, with condo values showing some of the steepest year-over-year declines. Condo apartments averaged $620,479 across the GTA, down roughly 9% from March 2025, despite a rebound in sales activity. This suggests that demand is returning selectively, but only where pricing reflects current market realities.

“Buyers continued to benefit from substantial negotiating power on price across major market segments in the last month. This explains why benchmark and average selling prices were down year-over-year. However, if market conditions continue to tighten, as they did in March, selling prices could start levelling off as we move through the remainder of 2026,” said TRREB Chief Information Officer Jason Mercer.

Within the City of Toronto, the picture was similarly nuanced. The average selling price rose modestly on a month-over-month basis to $1,022,874 yet remained 7.9% below March 2025 levels. Toronto sales were up only marginally year over year, and the decline in median price suggests that the monthly improvement in the average was not broad-based. In practical terms, this means buyers are still very discerning. Well-priced properties continue to attract attention, but aspirational pricing is meeting resistance, particularly in segments where there is more choice.

Another important theme in March was seller behaviour. Typically, this time of year sees a stronger wave of new listings as homeowners look to take advantage of the spring market. This year, that surge was notably absent. Some of this may reflect a reluctance among sellers to list in a market where values remain below prior peaks, while broader geopolitical and economic uncertainty has likely added another layer of hesitation. The result is a market where supply is not building as quickly as many had expected, which could become more supportive of pricing if demand continues to gradually improve through the coming months.

For now, the March market tells a story of cautious improvement. The environment is healthier than it was at the start of the year, but it is still far from robust. Buyers have more confidence than they did in the winter, yet they remain price sensitive. Sellers are benefiting from somewhat tighter conditions, but success still depends heavily on accurate pricing, strong presentation, and a clear understanding of the competitive landscape. In short, the spring market has begun to find its footing, but this remains a market that rewards strategy and realism over optimism alone.