Momentum Builds as Toronto’s Market Recalibrates

The Greater Toronto Area (GTA) real estate market continued to show signs of gradual improvement in May, with activity strengthening from both April and the same period last year. While this is not yet a market characterized by broad price growth or aggressive bidding activity, the tone has shifted meaningfully from the hesitation that defined much of the first quarter. Buyers are returning selectively, inventory is being absorbed, and the balance between supply and demand is tightening in several neighbourhoods and property segments.

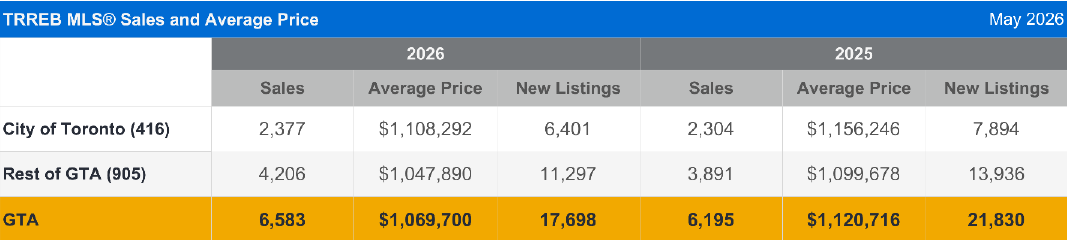

The Toronto Regional Real Estate Board (TRREB) reported 6,583 sales in May, a 6.3% increase compared with May 2025 and a 10.7% increase from April. This was one of the more encouraging elements of the month’s data, particularly because it was accompanied by a notable decline in new listings. There were 17,698 new listings brought to market in May, down 18.9% year-over-year. On a seasonally adjusted basis, sales were also up 10% from April, while new listings declined 2.1%, suggesting that the improvement was not simply the usual spring lift but a genuine firming in market conditions.

“Spring sales have been stronger than last year, reflecting improved affordability stemming from lower selling prices and borrowing costs. Sales are forecast to improve further as we move through the second half of this year. Recovery would be further bolstered by positive news on the trade front along with an easing of geopolitical tensions and related uncertainty,” said TRREB President Daniel Steinfeld.

Pricing continues to tell a more restrained story. The average GTA selling price in May was $1,069,700, down 4.6% from May 2025, though up 1.7% from April. The MLS® Home Price Index composite benchmark, which is often a better measure of underlying price trends, stood at $946,500, down 6.7% year-over-year and modestly higher month-over-month. In practical terms, this means activity has improved before prices have fully recovered. Buyers are more engaged, but they remain disciplined, value-conscious and highly responsive to pricing.

“Inventory levels trended lower over the past year, but buyers continued to have substantial negotiating power through the spring, helping with affordability. Looking ahead, if sales strengthen further relative to listings, selling prices will level off and even start to grow as we move into 2027,” said TRREB Chief Information Officer Jason Mercer.

The City of Toronto followed a similar pattern. Sales reached 2,377 in May, up 2.7% year-over-year and 2.8% from April. The average selling price in the city was $1,108,292, down 4.1% from last year but up 1.5% month-over-month. Active listings in Toronto were 15.3% lower than a year earlier, while new listings were down 18.9%. These figures point to a city market that is becoming firmer, though not overheated. Well-located, well-presented and accurately priced homes are receiving attention, while aspirational pricing continues to meet resistance.

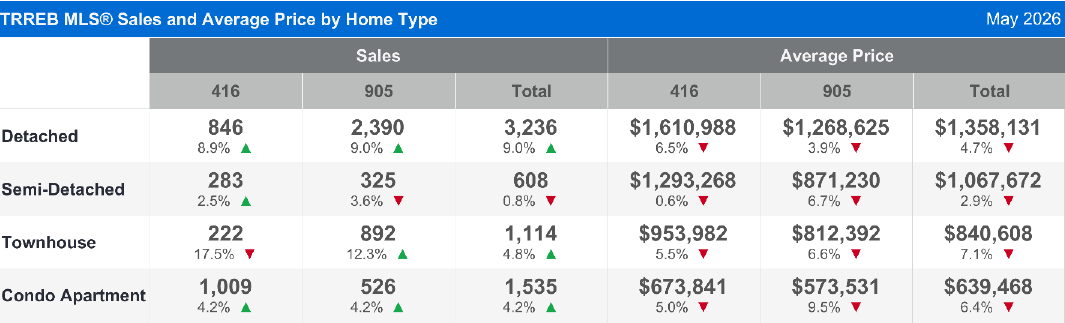

By property type, the low-rise market showed the clearest improvement in demand. Detached home sales in the GTA were up 7.9% year-over-year, reaching 3,236 transactions, even as the average detached price declined 4.7% to approximately $1.36 million. Semi-detached homes averaged roughly $1.07 million, down 2.8% year-over-year, with sales slightly below last year’s level. Freehold townhomes averaged approximately $916,000, down 8% year-over-year, although sales improved both monthly and annually. These figures underscore an important theme: buyers are active, particularly in the low-rise market, but they are not yet pushing prices higher across the board.

The condominium market remains the softest and most nuanced segment. GTA condo apartment sales totalled 1,535 in May, up 3.6% year-over-year but slightly lower than April. The average condo apartment price was approximately $639,000, down 6.4% from May 2025. This segment continues to be affected by affordability constraints, investor caution, elevated carrying costs and significant competition among listings. That said, the fact that condo sales improved compared with last year suggests that demand may be stabilizing, even if pricing remains under pressure.

One of the more notable improvements this spring has been market pace. In January, the average number of days on market was 45; by May, that had improved to 27 days. This does not mean properties are selling instantly, but it does show that appropriately priced homes are moving more efficiently than they were earlier in the year. Buyers may still be cautious, but they are prepared to act when they see value.

The broader economic backdrop remains central to the market’s recovery. The Bank of Canada has held its overnight rate at 2.25%, providing a measure of stability for borrowers after several years of interest-rate volatility. Lower borrowing costs compared with peak levels, combined with lower selling prices, have helped improve affordability at the margin. At the same time, many buyers remain sensitive to monthly carrying costs, employment uncertainty, geopolitical tensions and broader economic confidence.

Mortgage renewals are also shaping supply. Many homeowners who purchased or refinanced during the ultra-low-rate environment of 2021 are now renewing at materially higher rates. Yet, so far, this has not produced the wave of forced selling some had anticipated. The mortgage stress test, wage growth over the past five years and a general reluctance to sell into a softer price environment have all helped keep many potential sellers on the sidelines. In fact, some homeowners who may have considered selling appear to be waiting for stronger pricing conditions later in 2026 or into 2027.

For sellers, the May market offers a more constructive environment than earlier in the year, but it remains highly price sensitive. Presentation, preparation and pricing strategy matter. Homes that are positioned correctly are benefiting from improved demand and reduced competition compared with last year. Homes priced ahead of the market are still likely to sit, require reductions, or ultimately help sell competing properties.

For buyers, the opportunity has not disappeared. Prices remain below last year’s levels across all major property types, and negotiating room is still available in many segments. However, the window may be narrowing in certain neighbourhoods and property categories, particularly where quality inventory is limited. Buyers who are waiting for the absolute bottom may find that the best opportunities become less visible as confidence returns.

Overall, May was a positive step in the GTA’s market recalibration. Sales are improving, inventory is tightening, and pricing appears to be stabilizing after a prolonged period of softness. The market is not surging, but it is healthier than it was earlier this year. As we move into the second half of 2026, the key question will be whether improving demand, stable interest rates and lower inventory can translate into sustained price recovery. For now, the market remains balanced, selective and increasingly opportunity-driven for both buyers and sellers who are prepared to act strategically.